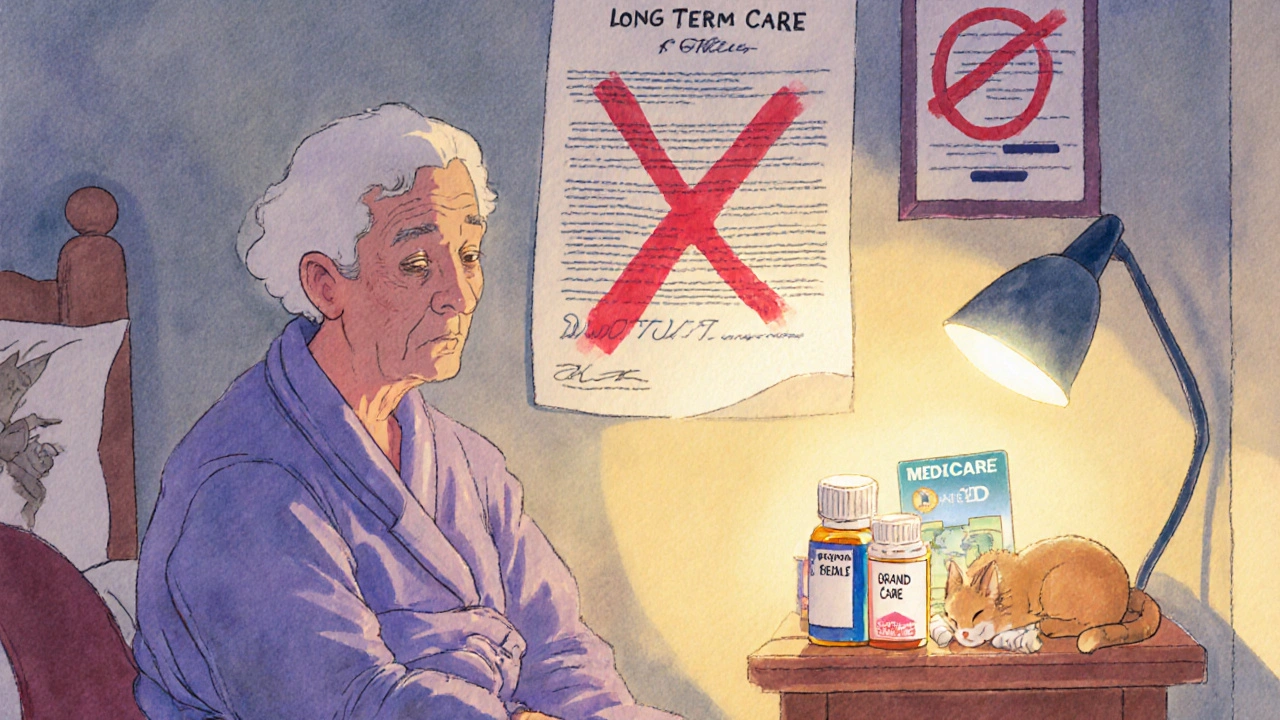

Many people assume that if they have long-term care insurance, it will pay for everything when they move into a nursing home - including their daily medications. That’s not true. And the misunderstanding can cost families thousands of dollars in unexpected out-of-pocket expenses.

Long-term care insurance covers room and board, help with bathing, dressing, and eating - the kind of daily support people need when they can no longer live independently. But it does not cover prescription drugs, whether they’re brand-name or generic. This is a hard rule, not a loophole. If you’re in a nursing home and taking pills for high blood pressure, diabetes, or arthritis, your long-term care policy won’t pay for them. Not one cent.

Who Actually Pays for Medications in Nursing Homes?

The real answer lies in Medicare Part D. By 2020, nearly 82.4% of all prescription drugs taken by nursing home residents were paid for by Medicare Part D plans. That’s more than four out of every five medications. Medicaid covers another 11.2%, and the rest come from private insurance, the VA, or the resident’s own pocket.

Here’s how it works: When someone enters a nursing home, the facility checks which drug plan they’re enrolled in. If they’re on Medicare Part D - which most are - the pharmacy bills the plan directly. The resident pays a copay, usually lower for generic drugs. A generic version of a common blood pressure pill might cost $5, while the brand-name version could be $40 or more. That’s why most nursing homes push for generics whenever possible - they’re cheaper, equally effective, and better covered.

Why Long-Term Care Insurance Doesn’t Cover Drugs

This separation isn’t an accident. It was built into the system on purpose. When long-term care insurance was created in the 1970s, lawmakers decided it should cover custodial care - the non-medical help people need as they age. Medical care, including doctor visits and prescriptions, was left to Medicare, Medicaid, or private health insurance.

The 2003 Medicare Prescription Drug, Improvement, and Modernization Act made this even clearer. It created Medicare Part D, which officially took effect in January 2006. Before that, millions of seniors in nursing homes had no drug coverage at all. Now, Part D is the backbone of medication access in these facilities. Long-term care insurers don’t cover drugs because they don’t have to - Medicare Part D already does.

Formularies and the Hidden Barriers to Generic Drugs

Just because Medicare Part D covers generic drugs doesn’t mean every resident gets them easily. Each Part D plan has a formulary - a list of approved medications. Not every generic is on every list. Some plans restrict certain drugs, require prior authorization, or charge higher copays for even common generics.

For example, a nursing home resident might need a specific generic antibiotic. If their Part D plan doesn’t include it, the pharmacy can’t fill the prescription until an exception is approved. That process can take days. In 2021, CMS required plans to approve non-formulary drug requests for nursing home residents within 72 hours - but delays still happen, especially in rural areas where fewer pharmacies contract with Part D plans.

And here’s the catch: Part D plans are not required to cover a drug beyond 180 days if it’s not on their formulary. That means a resident might get a needed medication for six months - then suddenly be denied. Families often don’t realize this until the pills stop arriving.

The Administrative Nightmare for Nursing Homes

Nursing homes don’t just deal with one drug plan. They manage dozens - sometimes over 20 different Part D plans among their residents. Each has its own rules, formularies, and prior authorization requirements.

A 2019 survey found that 78% of nursing facilities spend 10 to 15 hours a week just managing prescription drug coverage. That’s over 700 hours a year per facility. Staff time alone costs an average of $28,500 annually. Many facilities now hire dedicated pharmacy liaisons or use electronic systems that sync with Part D formularies to cut down on delays. Those that do see medication access times drop from 3.2 days to under a day.

It’s not just about speed - it’s about safety. A delayed antibiotic or insulin dose can lead to hospitalization. And hospital stays? Those are covered by Medicare Part A, not long-term care insurance. So the cost of a missed pill can spiral quickly.

What About People Without Drug Coverage?

Even today, nearly 9% of long-stay Medicare enrollees in nursing homes have no detectable drug coverage. They either didn’t enroll in Part D, lost their coverage, or their plan doesn’t work with their facility’s pharmacy. These residents pay out of pocket - or rely on temporary assistance from charities or state programs.

Studies show they get far fewer prescriptions than those with Part D. One 2020 study found that residents without drug coverage received 30% fewer medications on average. That’s not just inconvenient - it’s dangerous. A person with dementia who skips their Alzheimer’s meds, or someone with heart failure who misses their diuretic, can deteriorate rapidly.

What’s Changing in 2025 and Beyond

Good news: The Inflation Reduction Act of 2022 is making things better. Starting in 2025, Medicare Part D beneficiaries will pay no more than $2,000 out of pocket for drugs in a year. That’s a huge win for people who take multiple medications.

Also, Medicare will now cover all vaccines recommended by the CDC at no cost. And there’s growing pressure to standardize formularies across Part D plans - especially for nursing home residents. Some experts are pushing for a single, simplified formulary for long-term care, which would cut administrative chaos.

But challenges remain. Rural nursing homes still struggle to find pharmacies that work with all major Part D plans. Twenty-two percent of rural facilities report difficulties, compared to just 8% in cities. And while generics make up 90% of prescriptions, they only account for 25% of total drug spending - meaning the system still favors expensive brand-name drugs in some cases.

What Should You Do?

If you or a loved one is considering long-term care insurance:

- Understand what it covers - and what it doesn’t. Medications are not included.

- Make sure you’re enrolled in Medicare Part D. If you’re not, sign up as soon as possible. Late enrollment penalties apply.

- Ask which generic drugs are on your Part D plan’s formulary. Don’t assume all generics are covered equally.

- If a medication is denied, file for an exception. Nursing homes can help with this process.

- Check if your facility has a dedicated pharmacy liaison. If not, ask how they handle drug coverage delays.

Long-term care insurance is valuable - but it’s not a magic wand. It pays for care, not drugs. The real protection comes from Medicare Part D. Know your plan. Know your formulary. And don’t let a misunderstanding leave you without the pills you need.

Does long-term care insurance cover generic drugs in nursing homes?

No, long-term care insurance does not cover any prescription drugs, including generics. It only pays for custodial care like help with bathing, dressing, and eating. Medications are covered by Medicare Part D, Medicaid, or private health insurance.

Who pays for medications in nursing homes?

Medicare Part D pays for about 82% of prescriptions in nursing homes. Medicaid covers around 11%, and the rest come from private insurance, the VA, or out-of-pocket payments. Most residents are dual-eligible for Medicare and Medicaid, and their drugs are billed through Part D.

Why are generic drugs preferred in nursing homes?

Generics are chemically identical to brand-name drugs but cost far less. Medicare Part D plans offer lower copays for generics, so nursing homes and pharmacies prioritize them to reduce costs and improve access. About 90% of prescriptions in nursing homes are generics.

What if a needed generic drug isn’t on my Part D plan’s formulary?

You can request an exception. The nursing home’s pharmacy or your representative can file a formal appeal. Medicare Part D plans must respond within 72 hours for nursing home residents. If approved, the drug will be covered. If denied, you can appeal again or switch plans during open enrollment.

Can I switch Medicare Part D plans if I’m in a nursing home?

Yes. You can change your Part D plan during the Annual Enrollment Period (October 15-December 7) or during a Special Enrollment Period if your current plan doesn’t cover your medications or doesn’t work with your facility’s pharmacy. Nursing homes can help you compare plans and make the switch.

What happens if I don’t enroll in Medicare Part D?

You’ll pay full price for all prescriptions out of pocket - which can cost hundreds or even thousands of dollars a month. You may also face a late enrollment penalty if you sign up later. About 9% of nursing home residents currently have no drug coverage, and they’re at higher risk for medication gaps and health decline.

9 Comments

Elizabeth Grant

So many families get blindsided by this. I watched my grandma go from independent to needing 24/7 care, and we thought the insurance would cover her meds too. Turns out we were paying $300/month out of pocket for her diabetes pills. Long-term care insurance is great for baths and meals, but not for pills. Medicare Part D is the real MVP here.

angie leblanc

they say part d covers it but what if ur plan dosnt have the generic u need and the pharmacy is 40 mins away and the nurse says ‘well u gotta wait’ and then the med runs out and u get sicker and then they bill medicaide for the hospital stay?? who’s really profitin here??

LaMaya Edmonds

Let’s be real - this isn’t a gap in coverage, it’s a design flaw baked into the American healthcare system. Long-term care insurance was never meant to be comprehensive. It was designed as a luxury product for the middle class to avoid Medicaid spend-down. Meanwhile, Medicare Part D? A patchwork of 800+ private plans with 800+ formularies, each with their own bureaucratic landmines. The fact that nursing homes spend 700+ hours a year just navigating this mess? That’s not inefficiency - that’s systemic sabotage dressed up as ‘choice.’

And don’t get me started on the 9% without coverage. That’s not ‘lack of enrollment’ - that’s neglect. These are people who can’t advocate for themselves. Their meds get delayed because a pharmacy liaison is overworked, or a formulary change happened in January and nobody told the facility. This isn’t healthcare. It’s insurance roulette with lives on the line.

The $2,000 cap in 2025? Nice. But it doesn’t fix the formulary chaos. It doesn’t fix rural pharmacy deserts. It doesn’t fix the fact that brand-name drugs still make up 75% of spending despite generics being 90% of prescriptions. Someone’s making money off this mess. And it ain’t the residents.

See Lo

Let’s analyze the data: 82.4% Medicare Part D coverage, 11.2% Medicaid, 6.4% other. The math is irrefutable. The system is not broken - it’s optimized for cost-shifting. Long-term care insurers deliberately exclude pharmaceuticals because they are not ‘custodial.’ This is not an oversight - it’s a contractual boundary enforced by federal regulation since 1970s. The 2003 MMA was the final nail - Part D was engineered to absorb this liability. What’s alarming is not the exclusion, but the lack of public awareness. 9% without coverage? That’s not negligence. That’s systemic failure masked as individual responsibility. And the 78% of facilities spending 10-15 hrs/week on prior auth? That’s a tax on institutional efficiency. The real scandal? No one’s auditing the formulary gatekeepers. Pharma reps are quietly steering formularies toward higher-margin drugs. It’s not incompetence. It’s profit architecture.

And yes - emoticons: 😔

Chris Long

Why should the government pay for old people’s pills? They lived their life, now they’re a burden. If you can’t afford meds, you shouldn’t have gotten old. Long-term care insurance isn’t supposed to cover drugs - it’s supposed to cover dignity. But dignity doesn’t come from free pills. It comes from self-reliance. This whole system is just socialism for the elderly. Let them pay. Or die. Either way, it’s not my problem.

Liv Loverso

Medicare Part D didn’t fix the problem - it just moved the pain from one pocket to another. We pretend we’re helping seniors by giving them ‘choice’ in drug plans, but choice means nothing when your formulary is a labyrinth designed by actuaries who’ve never held a pill bottle. The real tragedy? We’ve turned healthcare into a game of corporate bingo - where the prize is survival, and the cards are printed in invisible ink. Generics aren’t cheaper because they’re better - they’re cheaper because we’ve convinced ourselves they’re ‘good enough.’ But what if ‘good enough’ kills someone quietly over 37 days because their insulin was denied for a paperwork delay? This isn’t policy. It’s moral negligence dressed in bureaucratic jargon.

And the $2,000 cap? A bandage on a hemorrhage. It doesn’t fix the formularies. It doesn’t fix the rural pharmacies that don’t exist. It doesn’t fix the fact that a person with dementia might forget to file an exception. We don’t need more caps. We need a single, unified, human-centered system. Anything less is just cruelty with a spreadsheet.

Steve Davis

Yo I just want to say I’m so sorry you’re going through this. I’ve been there - my mom’s on three meds, one of them got pulled from her plan last year and we had to appeal for 11 weeks. She cried every night thinking she’d run out. And the nursing home staff? They’re amazing but overwhelmed. I cried too. I just want you to know you’re not alone. And if you need help filing an exception, I’ll send you my template. I’ve done it 3 times. You got this. 💙

Michelle Machisa

Just make sure you’re on Part D. If you’re not, sign up now. Late penalties are brutal. And ask your facility which generics they use - not all are covered the same. If a med gets denied, push for the exception. They’re required to respond in 72 hours. And if your pharmacy is slow, ask if they have a liaison. Most good facilities do. This stuff matters. Your meds keep you alive. Don’t let bureaucracy steal that.

Ronald Thibodeau

LMAO you people act like this is some secret. Of course LTC insurance doesn’t cover drugs. It’s not medical insurance. It’s like buying a car insurance policy and being mad it doesn’t cover gas. DUH. Part D’s been around since 2006. If you didn’t sign up, that’s on you. Stop crying about formularies - just switch plans during open enrollment. And for god’s sake, use generics. They’re 90% of prescriptions for a reason. Stop being lazy and read your plan documents. This isn’t rocket science.